GST Council had its meeting at New Delhi after a gap of more than 2 months on 21st July, 2018. After deliberating on various issues, the final decisions made by the council are as follows.

§ Rationalization of Rates - The list of 28% was pruned significantly with TVs, washing machine, fridge, vacuum cleaners and various other consumer items to be taxed at 18% now instead of 28%. Sanitary napkins have been exempted from GST and so has Rakhis, commerative coins, brooms etc. Detailed list for the same is yet to be announced.

§ Returns- In a marginal relief, the Council also approved quarterly GSTR 1 for suppliers having turnover upto Rs.5 Crores. Tax will still need to be paid monthly however. This will cover approximately 93% of the registered suppliers. The Council also considered single page forms 'Sugam' and 'Sahaj' to make compliance easier for businesses.

§ Reverse charge deferred - Provisions of reverse charge on purchases from unregistered suppliers has been deferred till Sept 30, 2019.

§ Registrations - The Council approved amendments in the GST law to allow a supplier to have multiple registrations of the same vertical in one state.

(a) Council also approved proposal for composition dealers to provide services uptoRs. 5 lakh or 10% of their turnover (whichever is higher).

(b) The Council has also decided to allow migration of persons registered under previous regime till August 31, 2019. No late fee would be levied on such returns.

(c) Suppliers who apply for cancellation would not be required to file returns once they submit the application for cancellation.

- E-way Bill - With the E-waybill being a hot topic last week, the Council focused on devising SOP on handling inadvertent errors in e-waybills and standardization of penalties across the state. Council also deliberated on incorporating RFID with GSTN to track movement of goods throughout the country.

- Other Issues

(a) ITC refund has been allowed to textile industry for inverted duty structure for purchases made after July 27, 2018.

(b) Threshold for registration is proposed to be increased from Rs. 10 lakhs to Rs. 20 lakhs for 6 north eastern states including Assam, Arunchal Pradesh, Meghalaya and Uttarakhand.

(c) Ecommerce operators would only be required to get registration and pay tax if their vendors are not registered.

- Taxability of Tenancy Rights

Recently the Government has clarified the taxability of transfer of tenancy rights under GST vide its circular no 44/18/2018 dated 2nd May, 2018. The issue involved was whether tenancy premium shall attract GST when stamp duty and registration charges are levied on the said premium. The Government has clarified that merely because a transaction or a supply involves execution of documents which may require registration and payment of registration fee and stamp duty, it would not preclude them from the scope of supply of goods and services and from payment of GST and thus it has clarified that consideration for the said activity shall attract levy of GST under para 2 of Schedule II which states that any lease, tenancy, easement, license to occupy land is a supply of service even if stamp duty value and registration charges are paid. It was also clarified that grant of tenancy rights in a residential dwelling for use as residence dwelling against tenancy premium or periodic rent or both is exempt as per notification no. 12/2017-Central Tax Rate.

- No change in the GST law for Agriculturists and other support services

Government vide press release on 28th May 2018 has clarified that certain reports andnewsregarding change in GST law relating to farmerthat they would berequired to take registration and pay GST at the rate 18% if they lease out their land are incorrect and misleading. Further, it was clarified that support services to agriculture are also exempt since the GST is rolled out and it includes services incidental to it like renting or leasing of vacant land with or without structure incidental to it uses and agriculturists are also exempted from taking GST registration.

- Recipient is liable to pay tax under Reverse Charge on purchase of Priority Sector Lending Certificate

The Central Government vide Notification No. 11/2018-Central Tax (Rate) dated 28th May, 2018 has amended the Notification No.4/2017-Central Tax (Rate), dated the 28th June, 2017 by inserting S.no. 7 which has provided that on supply of Priority Sector Lending Certificate by a registered supplier, tax shall be payable under reverse charge mechanism by the recipient of such supply who isregistered under GST. Priority Sector Lending is an important role given by the Reserve Bank of India (RBI) to the banks for providing a specified portion of the bank lending to few specific sectors like agriculture, education, social infrastructure etc. (i.e. 40% of their total loans).Priority Sector Lending Certificates are certificates issued by banks that have overreached their priority sector lending targets given by RBI.Buyers of PSLCs are usually those banks who could not meet their priority sector lending targets.

- E-way Bill updates

- E-way Bill system for intra-state movement of goods are compulsory in every state except Delhi from 3rd June, 2018. However E-eay bill operations are compulsory for inter-state movement of goods in all states.

- The railways shall not deliver the goods unless the E-way Bill is produced at the time of delivery.

- If the goods transit through a second state while moving from one place in a State to another place in the same State, an E-way bill is required to be generated.

- West Bengal government has enhanced intra-state E-way bill threshold to Rs.1,00,000/- w.e.f. June 6, 2018 (without passing through any other state) vide Notification No. 13/2018- CT/GST.

The courts have been flooded with litigation on GST with lots of issues in the implementation of GST. We are sharing some key decisions of various High Courts on such matters.

- Fresh application for GST Registration can be filed subsequent to rejection of earlier registration application on account of discrepancies in documents

Rajeevan V.N. (Petitioner) filed a registration application under Goods & Services Tax but unfortunately his application got rejected on account of failure to provide explanation for discrepancy in documents submitted by him. Aggrieved by the same he filed a writ petition before the Hon’ble Kerala High Court.

Considering the submissions Kerala High Court held that an applicant whose application for GST registration has been rejected previously may subsequently file a fresh application for obtaining registration.

- Non filing of Form GST TRAN-1 due to technical glitches on the GST portal cannot be a reason to disallow the transitional credit

Despite his best and continued efforts M/s KTL (P) Ltd (Petitioner) was unable to file GST TRAN-1 on the last date i.e. 27th December, 2017 because the electronic system of GSTIN did not respond and thus suffering the loss of eligible transitional credit. The assessee thus filed a writ petition for the same.

Considering the relevant facts of the case the Allahabad High Court directed to reopen the portal so that GST TRAN-1 could be filed. However, in case the portal is not reopened, the department shall accept the application of the assessee manually and pass orders on it after due verification of the credits claimed. Thus, Non-filing of Form GST TRAN-1 due to technical issues may not be a reason to disallow the transitional credit that an assessee would be entitled for.

Note: - The Central Board of Indirect Taxes and Customs has set-up an IT Grievance Redressal Mechanism to address the grievances of taxpayers due to technical glitches on GST portal. Such grievances may relate to filing of any return or form as prescribed under the law or amending any form or return already filed (Refer Circular No. 39/13/2018-GST dated 03.04.2018).

- Penalty and seizure under Goods & Services Tax is not sustainable for movement of goods without e-way bill unless there exists malafide intention to evade taxes

Trade is facing difficulties in generating and downloading E-way Bill and applicability of E-way Bill under GST is not clear to many. One such victim was M/s Raj Iron & Building Materials (Petitioner- Assessee) who failed to generate E-way Bill for the movement of goods on account of inter-state inward supplies. Consequence of which the said goods a seizure order was issued for such non-compliance proposing to levy penalty on the grounds that goods are not were not accompanied with E-way Bill.

Accordingly, the Hon’ble Allahabad High Court allowed the writ petition filed by the assessee and set-aside the seizure order as non-sustainable. Holding that the penalty for non-compliance with e-way bill provisions without any intention to evade the payment of taxes is not sustainable.

- Cancellation of tenders awarded in pre-GST regime but not yet accepted by the participant for tender on account of introduction of GST cannot be said to be illegal or arbitrary

Nirmal Contructions (the petitioner-assessee) was one of the participants for a tender invited by The State of Madhya Pradesh Government(the Respondent) and was awarded such tender pending letter of acceptance. However, with the introduction of GST the government decided to cancel the contract so that future contracts should be invited excluding GST. The petitioner however aggrieved by such decision, filed a writ petition as against the action of the Government.

After carefully analysing the facts of the case MP High Court held that communication made to the Petitioner-Assessee for cancellation of the tender on account of introduction of GST is not illegal or arbitrary. Since the acceptance of the offer is not communicated to the Petitioner-Assessee, it cannot be construed as a concluded contract. In the absence of concluded contract, the Petitioner-Assessee cannot claim right to seek grant of contract only on the basis of the offer submitted by the Petitioner-Assessee at one stage.

- Courts cannot interfere Policy formulation for bringing petrol and diesel within the ambit of Goods & Services Tax

Petrol & Diesel are not within the ambit of Goods & Services Tax but Section 9 of the CGST Act, 2017 provides that petroleum and diesel would be brought within the ambit of GST from such date as the GST Council may deem fit and issue a notification in this regard. Aggrieved by the increase in prices of petrol and diesel within the country K.K. Ramesh (Petitioner in the given case) submitted a representation to The Union of India, The Secretary, Office of the GST Council Secretariat, New Delhi And The Commissioner, Commercial Tax Officer, Cheupakkam, Chennai for bringing such commodities into the GST net. However, when no response was received, he was constrained to approach The Madras High Court by filing a writ petition.

The Madras High Court held that the court is not in a position to issue any positive direction to the Respondents since it is for the Central Government to act on the recommendations of the Goods and Service Tax Council so as to bring the petrol and diesel within the ambit of the Goods and Service Tax net. It is a well-settled position of law that it is not for the Court to determine whether a particular policy or particular decision taken in the fulfilment of that policy is fair and a policy decision can be interfered with only if it is found to be arbitrary or based on an irrelevant consideration or malafide or against any statutory provisions.

The Government may notify the levy of GST on petroleum crude oil, high speed diesel, motor spirit (commonly known as petrol), natural gas and aviation turbine fuel on the recommendation of the GST Council. This being a policy matter, courts cannot interfere.

- DISCLAIMER:

The information is being shared on the basis of our reading and understanding. The usres of such information are required to confirm and verify the same independently before acting upon it. VJA shall not be liable for any defaults due to any actions taken on the basis of the above information.

The 27th meeting of the GST Council was held on 4th May, 2018 chaired by the Union Finance Minister Arun Jaitley at Prime Minister’s Office at New Delhi. The major items before the Council was the simplification of the returns without abandoning the invoice wise matching of input tax credit and the ownership of GSTN. Another issue was the implementation of sugar cess and how to improve compliance to the law. With the agenda of this meeting being limited to few items, the meeting was held through video conferencing. After deliberations, the Council laid down few recommendations under Goods & Services Tax which have been discussed as below.

Simplification of Returns

One of the major recommendation in this meeting was the simplification of returns under GST. Under the new process, there will be one Single return per month for the tax payers with exception to Composition and NIL taxpayers who will continue to file return on quarterly basis. Return filing dates shall be staggered based on the turnover of the registered person to manage load on the IT system and the Council has also recommended reduction of content/information to be filled in the return.

In case of B2C, the new return will contain the details of total turnover and in case of B2B invoice-wise details is required to be uploaded by the supplier along with HSN codes and taxes will be calculated automatically by the system. Monthly invoice matching of the details uploaded by the supplier would start around April 2019. For initial 6 months after implementation of new model for filing of returns under GST credit will be allowed to buyer on provisional basis. However, after 6 months of this step, the credit would be allowed to buyer only upon filing of return by the supplier and payment of tax. Such model of filing single monthly return would reduce the compliance burden significantly from the multiple filings currently required in a month but at the same time will leave the buyers on the mercy of suppliers to avail input tax credit. In order to avoid misuse of credit, in case the supplier defaulted in payment of tax the unloading of invoices shall be blocked above a threshold amount. Restricting the buyer from uploading the missing invoices or to take provisional credit may lead to losses for businesses where suppliers are not traceable and taxes has been paid to them. It might impact cash flows of the businesses on account of delayed credit in case of delay in uploading of invoices by the supplier. But there is one sigh of relief for the buyers that there will be no reversal or recoveries from the buyers on non - payment of tax by the suppliers.

The recommended system of return filing is quite similar to proposal made by Nandan Nilekani, (non-executive chairman of Infosys) to simplify the current process of complex return filing operations. As per his ideology in case the supplier does not upload sale invoice, nobody will buy from him since they won’t be getting any input credit from the purchase.

Ownership of GSTN

One more agenda item was to change the ownership structure of the GSTN. The original structure of GSTN was that 49% was held by the government i.e. 24.5% each by State & Central Government. And the balance 51% was held by some other entities. Finance Minister Arun Jaitley however proposed that this shareholding of 51% should be purchased by the government and divided equally between the States and the Centre. The council discussed the proposal at length and it was agreed that the 51% held by these private entities should be taken over by the government and eventually the Central Government should hold the 50% and the State Governments will hold 50% collectively. The collective share of the State Governments will be pro-rata divided among the states in accordance with their GST ratios. While doing so the council also recommended that the GSTN will continue to employ people contractually and have the flexibility to get the best talent on the best terms from the market considering the wide range of the activities and responsibilities of the GSTN.

Incentive for Digital Payments

The next important item of the agenda was with regard to an incentive on digitized payments. The issue before the council was whether digital payment either through banking mode or cheque mode or any form of digitized mode a 2% incentive should be given for those who pay entirely in the digitized mode. This will be subject to a cap of Rs 100 per voucher and this would not apply to the composition dealers. There was very detailed discussion held on this point, with the majority being in favour of this suggestion. There were two alternative views, one did not favour this and the second view was to accept this but to have a list of negative items on which this incentive would not be applicable. Therefore, council after a detailed discussion decided that a committee of 5 members i.e. 5 ministers of the State shall be constituted which would expeditiously consider all the view points and its recommendations would come up before the council in the next meeting for consideration.

Sugar Cess

The next item before the agenda was the imposition of a cess on sugar particularly considering that the cost of sugar has risen beyond Rs 35/Kg and the market price is between Rs 26 to 28/Kg and the sugarcane farmers are in deep distress and therefore whether the Council should some kind of a cess. Now, since this is after GST has been constituted, the first such suggestion has been come up how are such contingencies should be addressed in the GST regime, are they to be addressed by imposition of a cess or by increasing the tax amount or by some alternative method of revenue raising. These viewpoints were extensively discussed and debated in the council and it was agreed that an another separate group of 5 ministers be formed within the next 2 weeks because of the urgency of this matter would make a recommendation to the Council as to what are the avenues of raising revenue to meet contingencies of this kind where the cost of a commodity is much higher than its selling price and therefore the farmer is in distress and which are the cases in which this can be made applicable on a matter of principle itself.

GST Authority for Advance Ruling has become fairly active recently with a slew of judgements coming in the last few days. We have compiled below the key judgements announced recently for quick reference.

- Sale of Duty Free Shops taxable under GST

The Delhi AAR has recently ruled that the sale of goods by the Duty Free Shops at international airports is taxable under GST. The Authority ruled that while such supply may be taking place beyond the customs frontiers of India under IGST Act butthe said Shops are within territory of India under the CGST Act. Consequently, sale of goods by such shops cannot be treated as export and hence chargeable to GST.

- Mandatory registration in case of RCM under 9(3)

West Bengal AAR has clarified that registration is required to be obtained even if the assessee has only exempt turnover but has liability under reverse charge under Section 9(3).

The Applicant is not required to be registered under the GST Act if he is not otherwise liable to pay tax under reverse charge under section 9(3) of the GST.

- Intermediary Services provided to University Abroad – Not Qualified as exports.

In the case of services for promotion and assistance in recruitment of students for a foreign university, the WB AAR has held that the applicant’s primary service is to recruit/enroll students for the foreign university. Promotion of courses is an incidental & ancillary activity to the principal supply and applicant is paid consideration in the form of commission based on performance in recruiting students, as a percentage of the tuition fee collected from the students

The applicant is an intermediary service provider hence place of supply should be according to Sec 13(8)(b) of the IGST Act 2017. Thus, place of supply falls within India and conditions of Export of services does not qualify and the transaction becomes taxable under the GST Act.

- No GST on goods brought and sold outside India

Kerala AAR has clarified that neither GST is leviable on sale of goods procured from other country and directly supplied to recipient country nor stored in warehouse of that country, as the goods are not imported into India at any point. The goods are liable to IGST when they are imported into India i.e. they are bought into Indian Territory.

- GST on food to employees from canteen in office premises

In its order, the AAR Kerala has clarified that even though there is no profit on the supply of food to employees, there is "supply" as provided in Section 7(1)(a) of the GST Act, 2017 and hence recovery of food expenses from the employees for the canteen services provided by company would come under the definition of 'outward supply' as defined in Section 2(83) of the Act, 2017, and therefore, taxable as a supply of service under GST.

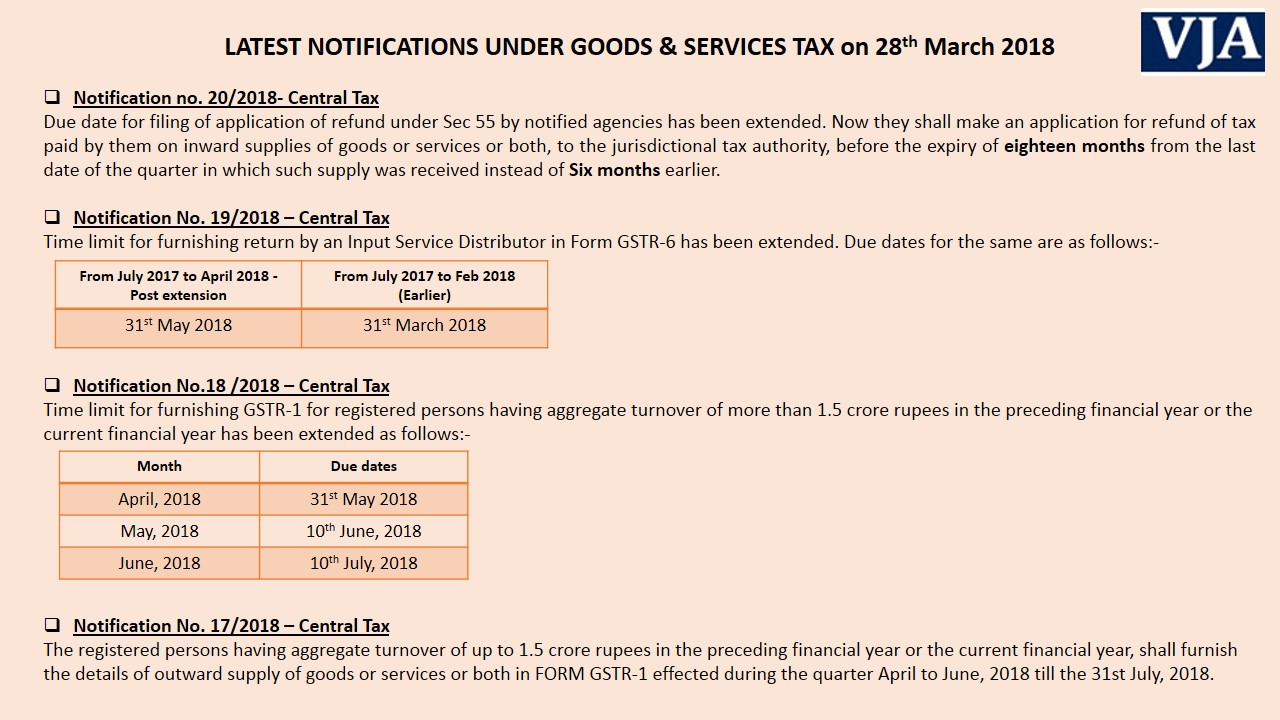

- Notification No. 17/2018 - Time limit for furnishing details of outward supply of goods or services or both for persons having turnover upto 1.5 crores

- Notification No. 18/2018 - Exstension of time limit for furnishing GSTR-1 for persons having turnover more than Rs.1.5 crores

- Notification No. 19/2018 - Extension of time limit for furnishing return by Input Service Distributor in Form GSTR-6

- Notification No. 20/2018 - Extension of time limit for filing application of refund under Section 55

Further Reading

Further Reading{kind=link}

E-way Bill Rules updated

The Government has amended the E-Waybill rules after various challenges were faced during the first attempt made on February 1, 2018. The key changes made are as follows:

1.Details can now also be furnished by transporter in Part A of Form GST EWB 01 after receiving authorization from the registered person.

2.E-commerce operator or courier agency can furnish information in Part A of Form GST EWB 01, after taking authorization from consignor, if goods are transported through e commerce or courier agency.

3.In inter-state movement of goods by principal to job worker, Job worker (if registered) or principal shall generate the e-way bill without any limit. Earlier only principal had the liability to generate E-way Bill.

4.For determining value of consignment, value of exempt supply shall be excluded.

5.Even if goods are transported via road through Public conveyance for example, Bus, cab, etc, the consignor or the consignee is required to generate E-way Bill.

6.In case of transportation of goods via railways, railway shall not deliver the goods unless E-way bill is produced at the time of delivery.

7.If goods are transported from consignor place to transporters place within a State or UT for further transportation and distance is up to 50 km , then the transporter may not furnish the details of conveyance in Part-B of Form GST EWB -01. (Earlier limit was 10 km)

8.Details of conveyance not required to be updated in case, if goods are transported from transporter place to consignee place and distance is up to 50 km within a state or Union Territory. (Earlier limit was 10 km).

9.Unique number shall be valid for 15 days instead of 72 hours for updation of Part B of Form GST EWB-01.

10.Validity period of E-way Bill for over dimensional cargo has inserted, which is upto 1 day upto 20 kms and one additional day for every 20kms or part thereof thereafter. “Over Dimensional Cargo” means a cargo carried as a single indivisible unit and which exceeds the dimensional limits prescribed in Rule 93 of Central Motor Vehicle Rules, 1989, made under the Motor Vehicles Act, 1988.

11.List of exceptions to requirement of E-way bill has been lengthened by few more insertions such as – where goods are being transported – (i) under customs bond from an ICD or CFS to a customs port, airport, air cargo complex and land customs station, or from one customs station / port to another customs station / port, or (ii) under customs supervision or under customs seal, where the goods being transported are transit cargo from or to Nepal or Bhutan, any movement of goods caused by defence formation under Ministry of defence as a consignor or consignee, where the consignor of goods is the Central Government, Government of any State or a local authority for transport of goods by rail, where empty cargo containers are being transported, etc.

The GST Council held a brief meeting today at Vigyan Bhawan, New Delhi. While there was a big hype expecting simplification of returns in this meeting, the Council could not come to a consensus on the same. An implementation committee has been proposed to finetune the IT Processes and to address the grievances being faced by the taxpayers. The Council also extended various exemptions which were due to expire on the 31st of March, 2018. Some of the key decisions made at today’s Council meeting are as follows.

Ø The present system of filing of GSTR-3B and GSTR-1 is extended for another 3 months till the new return system is finalized.

Ø Exemption on payment of tax on reverse charge basis for supplies from unregistered suppliers has been further continued till 30th June, 2018.

Ø The provisions for TDS and TCS shall also remain suspended till 30th June, 2018.

Ø E-way bill Rules as notified on March 7, 2018 have been ratified by the Council. E-way bill for inter-State movement of goods shall be introduced from 01st April 2018.

Ø For intra-State movement of goods, e-way bill system will be introduced w.e.f. a date to be announced in a phased manner but not later than 01st June, 2018.

Ø GST implementation Committee (GIC) has been tasked with the work of redressing the grievances caused to the taxpayers arising out of IT glitches.

Ø Benefit of various export promotion schemes, 0.1% scheme for merchant exporters and recognition of various schemes as deemed exports have been extended upto 01st October, 2018.

Ø E-Wallet Scheme for exporters has been deferred to 01st October, 2018 from April 1, 2018.

Ø Variance between self-declared liability in FORM GSTR-1 & FORM GSTR-3B and between taxes paid at the customs and credit taken in GSTR-3B has been significant. A committee to analyse the same has been formed.

Decisions at GST Council's Meeting on the 18th of January, 2018

The GST Council held its 25th meeting at Vigyan Bhawan, New Delhi and deliberated on various problems and challenges in respect of GST. The agenda of simplification of returns was taken up with presentations being made by Nandan Nilekani from Infosys on the subject. However, no clear concensus emerged today. The decision was deferred to the next meeting which is proposed to happen in the next 10 days. Some of the key highlights of the meetings are as below.

1. Process for simplification of return was reviewed. GST Council proposed to meet again on the January 28, 2018 to decide. The following process suggested.

- Form GSTR 3B to be continued. Uploading of invoices in the form of GSTR 1 to continue. Mismatches in claim to be handled at assessment level.

2. Declining GST Collections were reviewed and discussed. Ewaybill as an anti-evasion measure to be implemented. Hence, trial of Eway bill to continue till Jan 31, 2018. Interstate ewaybill to become mandatory from February 1, 2018. Other such measures to be considered.

3. Definition of handicraft items reviewed. Fitment committee to review the rates.

4. Rates and classifications for 29 Goods and 53 categories for services were reviewed. Rate list to be shared shortly. New rates to come into force from 25th of January, 2018. Expected that rate of used cars will be reduced.

5. Review of composition scheme was made given the declining revenues of the Govt. Collection from Composition scheme under Quarter 1 is only Rs. 307 Crores. Changes in composition scheme to be proposed in the next GST Council meeting. Reverse charge on purchases from unregistered suppliers to be applicable on composition suppliers.

6. Late fee for GSTR-1, GSTR-5, GSTR-5A reduced to Rs. 50 per day and Rs. 20 per day for nil filers. Late fee for GSTR-6 reduced to Rs. 50 per day.

7. Suppliers who had obtained voluntary registrations can apply for cancellation even before expiry of one year from date of regn. Duedate for cancellation of migrated registrations extended till March 31, 2018.

8. Modifications in Ewaybill rules proposed and will be notified shortly.

9. Itemwise list of change of tax rate is as per links below.

For Goods - http://www.pib.nic.in/PressReleaseIframePage.aspx?PRID=1517141

For Services - http://www.pib.nic.in/PressReleaseIframePage.aspx?PRID=1517139

As predicted by various news outlets, the GST council has finally provided relief to businesses of all size and types to alleviate the pain on ground. The key changes are as follows

1. The Turnover for composition scheme has been raised from ?75 Lakhs to ? 1 crores. Group of Ministers committee (GOM) formed to examine

a. whether Exempted goods should be excluded from turnover,

b. whether Interstate transactions allowed to composition dealers and

c. whether credit of tax paid by composition dealer supplier be allowed to his buyer.

2. The E-waybill provisions have been deferred till April 2018.

3. The provisions of Reverse charge on unregistered supplier have been suspended till 31.03.2018.

4. Biz with annual turnover of less than Rs. 1.5 Crores will be required to file returns on quarterly basis for October 2017 onwards. Credit to be provided to buyer on provision basis. Returns for July, Aug and Sept 2017 have to be filed on monthly basis.

5. Council has given in-principle approval for reducing the rates of AC restaurants to 12% from 18% possibly without ITC. GOM to examine the issue.

6. Provision for 'Deemed exports' @ 0.1% has been approved for merchant exporters.

7. Exporters (advance authorisation, 100% EOU, Star House) would not be required to be paid GST on import of goods for exports.

8. E-wallet system to be introduced from exporters from 1st April 2018.

9. Refunds for exporters for July 2017 and August 2017 input credits from Oct 10, 2017 on manual basis.

10. Service providers providing inter-state services and having turnover less than 20 lakh have been exempted from registration.

11. TDS and TCS provisions deferred till April 1, 2018

12. Rates reduced for various items and services. List includes Gas Stove, man made yarn, clips, pins, sliced diced mangoes, khakhra, unbranded namkeen, unbranded ayurvedic medicines, plastic, rubber or paper waste, flooring stones (other than marble and granite), stationery items, parts of pumps. For services, rates reduced for job work on zari, imitation jewellery, printing, high labour works contract services for govt contracts.

13. Relief provided for old car leases through abatement of 35% in value.

14. No tax to be paid on advances by goods supplier having turnover upto Rs. 1.5 crores